The credit market is vital to our global economy, and therewith also for our society. Served by the banking market over centuries, the increasing regulations like the Basel regime in Europe, now in the 4th revision, and the Capital Requirements Regulation (CRR), have led to tighter credit standards and significant decline of credit underwriting by the banks. Especially the real estate market is facing massive difficulties in financing and refinancing, also impacted by the overall pressure on the real estate market globally. CBRE estimates a refinancing gap of €176 Billion between 2024–2027 in Europe alone.

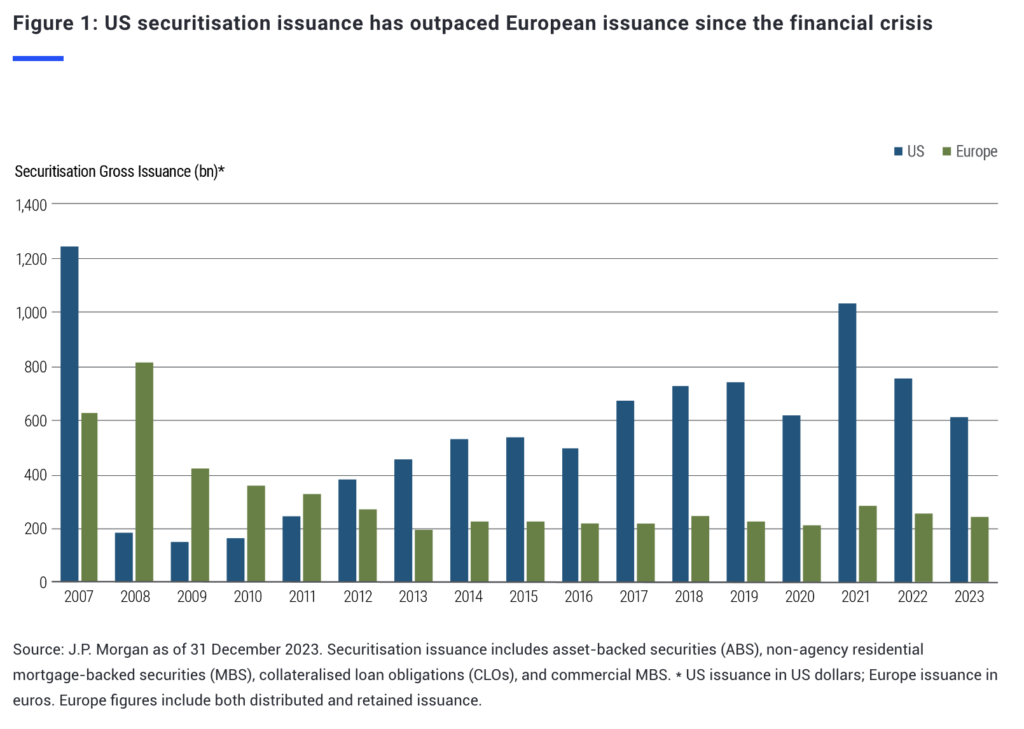

Other than in the US, where the securitisation is a major part of the debt financing market, the European securitisation market has declined from € 2 Trillion in 2007 to less € 1.2 Trillion in Q1/24 according to the latest AFME report of Q1/24 . This has partly to do with tighter regulations after the global financial crisis 2007/2008, as well as the cheap liquidity provided by central banks like the ECB to banks and the extremely low interest rates that made those products unattractive to investors. But we’re still talking about a Trillion Market.

But this is about to change. With the sharp rise of interest rates and therewith attractive yields for investors, alternative lenders such as private credit funds are closing the gap banks leaving in the market. But also banks are increasingly re-starting securitisation efforts as this offers also a great opportunity to offset their balance sheet a free up regulatory risk capital and expand their credit underwriting again.

The Growth of Asset-Backed Securities

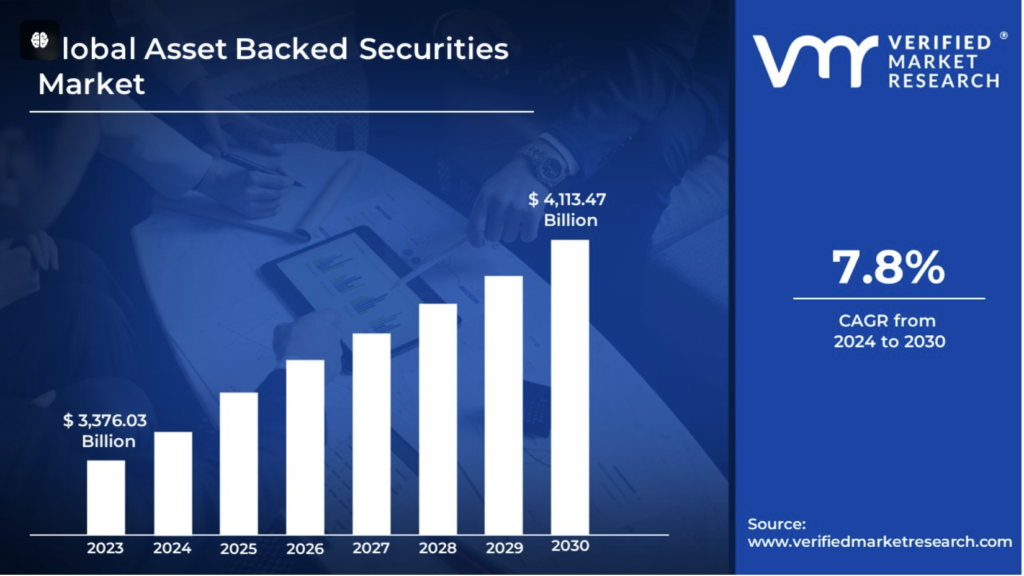

According to a report by Verified Market Research, the market for ABS as an overall term for Asset-Backed Securities, Mortgage-Backed Securities (MBS), Collateralised-Loan Obligations (CLO) and Collateral-Debt Obligations (CDO) is about to grow with a CAGR of 7.8% between 2023–2030.

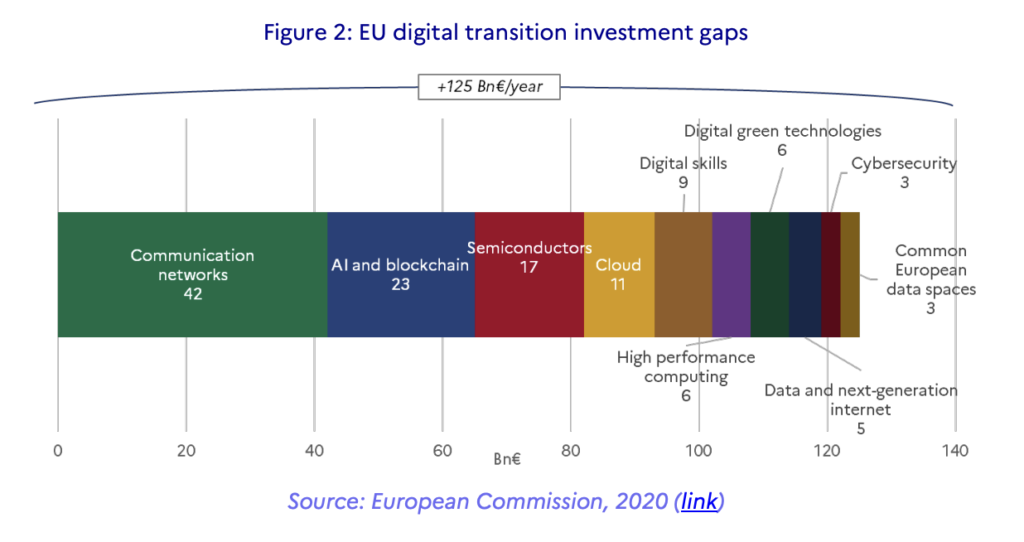

Since the capital market in Europe is trailing behind the US, the ESMA (European Securities and Markets Authority) entrusted a committee of experts with the mission of formulating concrete proposals to revitalise the Capital Markets Union (CMU) and in particular measures to support the revival of the ABS market, which is seen as a crucial element for the financial market as a whole.

Next to clear proposals to stimulate capital markets and revitalise the European securitisation market, their proposals also outlines the funding needs in innovative technologies, whereby AI and Blockchain take a big bulk of €23 Billion. It can clearly be said that the EU already in 2020 saw the potential of these technologies, also in the context of revitalising capital markets.

The Role of the Blockchain and Tokenisation in the Revival of the ABS Market

As we might all know, the GFC was triggered by the growing interest in those asset-backed securities by global investors and the irresponsible expansion of mortgage loans to sub-prime loans and moreover the lack of structuring and repackaging into opaque CDO’s.

The blockchain as a immutable decentralised single source of truth for data, combined with the extremely powerful analytical capabilities of AI, will offer greatest transparency and efficient risk analytics to avoid another similar effect like in the sub-prime crisis.

Tokenisation is poised to bring a revival in the realm of Asset-Backed Securities (ABS) including ABS, MBS, CLO’s and CDO’s. The cornerstones of the securitisation market. By leveraging blockchain technology, tokenisation addresses several longstanding issues especially in this market, and paves the way to unlock new potential for these investment products and a better capital market overall.

Enhanced Transparency and Trust

One of the primary challenges in the securitisation markets is the lack of transparency. The global financial crisis of 2007/2008 highlighted how opaque and complex these products could be, leading to significant mistrust among investors. Tokenisation revolutionises transparency by recording all underlying asset details, transactions and ownership changes on a distributed ledger (DLT). This immutable ledger provides real-time visibility into the underlying assets, their performance, potential risks and its trading history.

Investors can track the performance of single assets, asset pools, verify the legitimacy of the underlying assets, and gain confidence that their investments are secure. This increased transparency can restore trust in ABS and MBS products, attracting a broader range of investors and potentially leading to better valuations.

Improved Liquidity

Traditional ABS products often suffer from liquidity issues, especially in times of market stress. Tokenisation can significantly enhance liquidity, making this market more accessible, transparent and efficient on digital platforms. Investors can buy and sell tokens representing the full asset or fractions of an ABS, making it easier to enter and exit positions.

The nature of digital alternative marketplaces is a 24/7 operations providing continuous liquidity, reducing the need for intermediaries and lowering transaction costs. This increased liquidity can make ABS products more attractive to a wider range of investors, including those who may have previously been deterred by the illiquidity of these assets.

Democratisation of Investment Opportunities

Tokenization can democratise access to ABS products, traditionally the domain of big institutional investors. By creating transparent products in a simpler and more efficient structure, those products have a tremendous potential for other professional investors, in particular private debt funds, but also family offices, which typically engage in bilateral lending, facing high illiquidity of their investment. This democratization can broaden the investor base, increase market depth, and provide more capital for securitization transactions.

Moreover, tokenized ABS products can be offered on decentralised finance (DeFi) platforms, where those investors can deposit into risk-adjusted loan pools without the need for traditional financial intermediaries. This shift offers also for those investors alternative investment opportunities in Real-World-Assets (RWA) and provides the market additional liquidity.

Enhanced Efficiency and Cost Savings

The traditional process of issuing loans, structuring and trading ABS products involves numerous intermediaries, including banks, brokers, trustees, accountants and auditors, lawyers, paying agents, transfer agents, custodians, etc. Each adding complexity, costs, and delays. Tokenisation can significantly reduce complexity by streamlining issuance, settlement, and record-keeping through smart contracts on a blockchain. Smart contracts can automatically enforce the terms of the securities, such as interest payments and principal repayments, reducing the need for manual intervention. In fact Smart Contracts can, and ultimately will replace most of those service providers and intermediaries, as all data is on-chain and Smart Contracts executes actions according to fully transparent and auditable programable rules.

These efficiencies lead to significant cost savings, making it more economical to issue and manage ABS products. Lower costs can translate into better returns for investors and more competitive pricing for issuers, encouraging greater activity in the securitisation market.

Innovation and Customization

Tokenisation will clearly drive innovation in securitised products by enabling greater customisation and flexibility. Issuers can create bespoke tokenised securities tailored to specific investor preferences, such as different risk profiles, maturities, and payment structures. This flexibility can attract a broader range of investors with diverse investment goals and risk tolerances.

Furthermore, the programmability of blockchain technology can facilitate the creation of new types of structured products that combine features of traditional ABS with different asset classes. For example, hybrid tokens could offer exposure to both real estate and other private debt types, providing investors with unique diversification benefits.

Risk Management and Regulation

Tokenisation can also enhance risk management and regulatory compliance in the ABS markets. Blockchain’s transparency and traceability can improve monitoring and oversight, allowing regulators to better understand and manage systemic risks. Automated reporting and compliance features can ensure that tokenised securities adhere to regulatory requirements, reducing the likelihood of fraud and misconduct.

Additionally, the real-time data provided by blockchain technology can enable more accurate risk assessment and pricing of such products. Investors can make more informed decisions based on up-to-date information about the performance and quality of the underlying assets.

Undoubtedly, technology will usher new investment primitives and therewith new opportunities. For sure there are also risks, old one and new ones. It’s not about circumventing regulations like Basel 4 or Solvency 2, it’s quite the opposite. It’s about leveraging the potentials of technology to make the financial industry more efficient, transparent and resilient and manage global systemic risks better avoiding the next GFC and support the economy and the society better.

RIVA Markets as the Market Infrastructure for Tokenized ABS

At RIVA Markets we’ve early identified the potential of the Blockchain and AI in the private credit market and the revival ABS. The recent and foreseeable developments in the market, especially in the light of the ESMA proposal report, it just strengthens our opinion and work innovating this massive and important market, solving real problems as addressed.

“Our mission is to provide a novel capital market infrastructure and therewith a primary issuance and secondary market for ABS products leveraging the blockchain and AI.“

RIVA Markets includes for distinct and connected solution modules:

RIVA Prime

RIVA Prime is a powerful Loan Origination System (LOS) to originate loans directly on-chain and therewith create full transparency from origination and along its full lifecycle.

RIVA Prime

RIVA Securities is an integrated securitisation and tokenisation solution, offering direct digital securitisation through SPV Compartments and tokenisation in single loan tranche ABS & MBS (SASB — Single-Asset-Single-Borrower), loan pools for CLO’s and CDO’s or any other form of composable securities tokenisation.

RIVA Markets

RIVA Markets is our core and client facing module. A primary issuance and secondary trading marketplace for institutional and professional investors providing a global source of vetted deals, carefully prepared project and deal data, an integrated data room, an integrated AI Due Diligence tool to generate a due diligence report from and into different languages to overcome the language issue, a chat and negotiation function, a term sheet and contract generator with integrated digital signature through DocuSign integration and multiple Fiat and on-chain settlement methods, reducing transaction time by up to 90%.

RIVA Markets is also an all-in-one asset management solution, offering an integrated portfolio management with access to the on-chain application and transaction data. Our integration with Moody’s Analytics and Moody’s Rating provides additional deep-dive into the risks of the underlying asset(s).

Our secondary market enables investors on the one side to sell their assets, and secondary market investors on the other side a source of secondary deals with greatest transparency, which is also supporting the market to become more liquid.

A Solution for Private Market Investors and Banks alike

RIVA Markets is addressing private market investors such as private debt funds, real estate funds, pension funds, endowment funds, family offices, insurance as well as banks asset management divisions, but also banks for their securitisation of loan portfolios.

RIVA Securities has also been built to offer banks and non-bank loan originators a solution to bring their loan portfolios on chain, structure, securitise those loan portfolios and either sell directly to their investors network or list and trade them on RIVA Markets.

The Transition to Tokenized Asset Management and our Hybrid Approach

Although the market for tokenised asset management is growing fast, we’re aware that many institutional and professional investors are not ready yet to deal with tokens directly. That’s why our claim is “Transition to the Future of Tokenised Asset Management”. Hence, we’ve built a hybrid solution for simple bilateral loan agreements, securitised assets and settlement through depository accounts, but with on-chain loans, and the full tokenisation solution. We believe that this allows to leverage the benefits of the blockchain and smoothly transition over to the future of tokenised asset management without hurdles.

Working in Interoperability and Building a Global Network for Distribution and Liquidity

We’re convinced that the market can only flourish when we’re not an isolated market, but cooperating with other tokenised assets markets and institutions already operating their own marketplaces to exchange assets and leverage distribution and liquidity globally. This is why we initially built on the Provenance Blockchain and now integrating other technologies such as the ERC-3643 standard by Tokeny, and further deploying on multiple chains such as Polygon, Base, Avalanche and other EVM Chains offering enhanced privacy, as well as evaluating interoperability solutions such as Chainlinks’ CCIP in combination with Swift and Axelar.

In this sense we’re living the mantra

“We cannot predict the future but we can work on it”.